TL;DR:

- Insurance laws like the ACA, MHPAEA, and EPSDT ensure coverage for autism therapies including ABA.

- Medicaid often provides more comprehensive, unlimited coverage compared to private plans, depending on eligibility.

- Families should proactively document diagnoses, treatment plans, and appeal denials to access necessary autism care.

Autism therapy without insurance can cost your family $40,000 to $60,000 per year, and that number stops most families cold. Applied Behavior Analysis (ABA), which is the most widely prescribed behavioral therapy for autism spectrum disorder (ASD), runs between $120 and $200 per hour, often 25 to 40 hours per week. That is not a niche expense. That is a second mortgage. Yet millions of parents are navigating insurance paperwork, denial letters, and confusing state laws without a clear roadmap. This guide breaks down what insurance actually covers, how federal and state rules affect your access, and the practical steps you can take right now to protect your child’s care.

Table of Contents

- How insurance shapes access to autism therapies

- Comparing private insurance and Medicaid for autism care

- State-by-state differences and policy trends

- Smart strategies for getting the most from your insurance

- Why navigating insurance for autism care requires more than paperwork

- Find trusted autism therapy providers and support

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Insurance is essential | Coverage enables access to autism therapies that might otherwise be unaffordable for most families. |

| Medicaid vs private plans | Medicaid offers broad mandated benefits based on need, while private insurance may have therapy caps and tighter rules. |

| State policies matter | Coverage and access can vary dramatically by state due to differing mandates and fiscal policies. |

| Combine resources | Maximize care by using insurance together with school services, waivers, and advocacy resources. |

| Be proactive | Successful navigation involves early action, documentation, and response to policy changes and denials. |

How insurance shapes access to autism therapies

Insurance is not just a financial tool for autism families. It is often the difference between a child getting the early intervention they need and a family making impossible financial choices. Before you can advocate for your child, you need to understand the legal foundations that are supposed to protect you.

Two major federal frameworks define what insurers must cover:

- The Affordable Care Act (ACA): The ACA classifies behavioral health treatment, including ABA therapy for autism, as an essential health benefit (EHB) in all Marketplace and small-group plans. This means insurers cannot impose annual or lifetime dollar limits on these services, and they cannot deny coverage based on a pre-existing condition like ASD.

- The Mental Health Parity and Addiction Equity Act (MHPAEA): This law requires that mental and behavioral health benefits be provided on the same terms as medical and surgical benefits. In plain terms, if your plan covers unlimited physical therapy sessions, it cannot impose a hard cap of 20 ABA sessions per year without a comparable limit on medical visits.

- Medicaid’s EPSDT requirement: Early and Periodic Screening, Diagnostic, and Treatment (EPSDT) is a federal Medicaid rule that covers ABA and autism therapies for all children under 21 when deemed medically necessary. Unlike private plans, there are no age caps, no hour limits, and no dollar maximums tied to arbitrary formulas.

Important: Knowing these laws exist is powerful, but applying them requires documentation. Your child’s doctor plays a central role. A written diagnosis, a treatment plan, and a referral for medically necessary services create the paper trail that insurance companies must respond to.

You can learn more about how autism insurance parity rules are applied and what they mean in practice for your specific plan type. The legal baseline is clear, but navigating what happens between the law and your actual benefits statement takes more preparation.

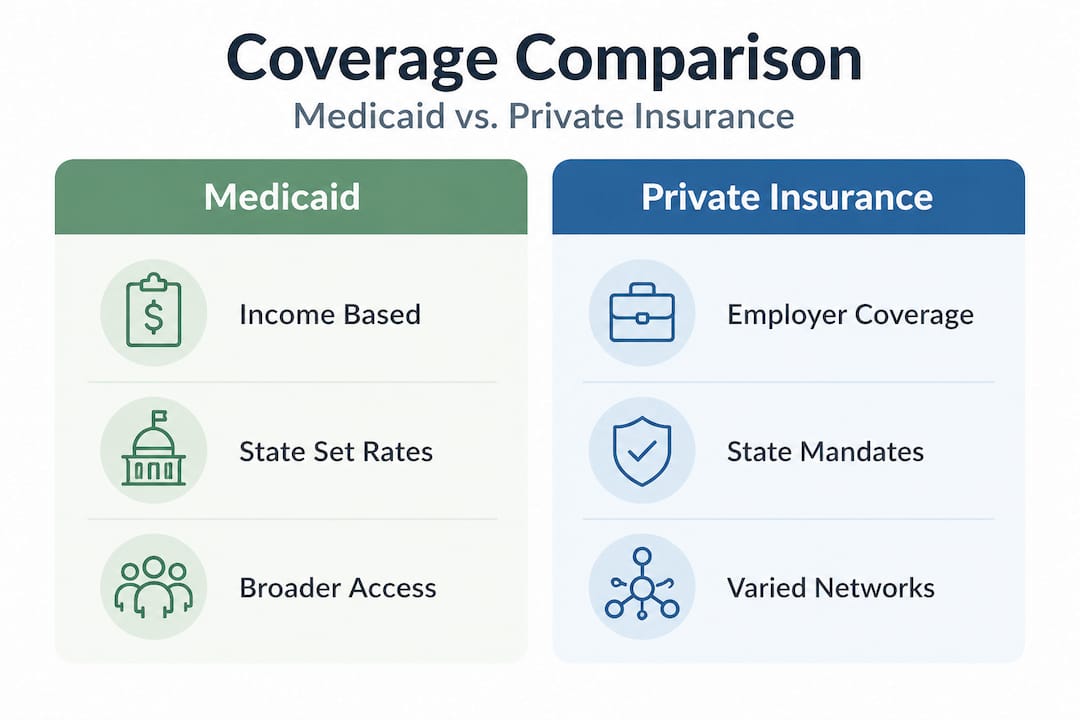

Comparing private insurance and Medicaid for autism care

Once you understand the laws, the next step is figuring out which insurance pathway works best for your family. Private insurance and Medicaid both reduce out-of-pocket costs dramatically compared to paying without coverage, but they work in very different ways.

| Feature | Medicaid | Private Insurance |

|---|---|---|

| Eligibility basis | Income and disability status | Employment or marketplace enrollment |

| Coverage limits | Based on medical necessity, not set caps | Subject to state mandates and plan caps |

| Cost to family | Little to no out-of-pocket | Deductibles, copays, and coinsurance apply |

| Provider network | Varies by state, can be narrow | Often broader but geography-dependent |

| Authorization process | Required but necessity-based | Often requires extensive prior authorization |

| Flexibility for hours | Unlimited if medically justified | Often capped by plan or state mandate |

The ABA therapy insurance coverage landscape shows that Medicaid is often the stronger option purely on paper. Under EPSDT, no hard therapy caps apply if your child’s treatment team can demonstrate medical necessity for a given number of hours. A child who needs 30 hours of ABA per week can receive exactly that without a plan automatically cutting it to 20.

Private insurance, by contrast, varies enormously. Many states have passed autism insurance mandates requiring private plans to cover ABA, but the strength of those mandates differs. Some states mandate robust coverage with high dollar caps. Others allow plans to limit weekly hours or impose strict diagnostic criteria before approving services.

Here is what the financial difference looks like in real terms. Without any coverage, a family paying out of pocket for 30 hours of ABA per week at $150 per hour spends roughly $4,500 per month, or over $54,000 annually. With Medicaid covering the full cost, that drops to near zero. With private insurance, a family might still owe their deductible (often $2,000 to $5,000) plus copays, but costs drop dramatically compared to uninsured rates.

Pro Tip: If your household income qualifies for Medicaid but you also have private insurance through work, do not drop your private plan automatically. Some families benefit from having both, using private insurance as primary and Medicaid as secondary to cover gaps like deductibles and copays.

State-by-state differences and policy trends

Federal law sets the floor, but states build the house. What your insurance actually delivers depends heavily on where you live, and the landscape is shifting fast.

Here is a snapshot of recent state-level trends that are directly affecting autism families:

- Medicaid spending surge: National Medicaid spending on ABA therapy jumped from $347 million to $2.2 billion, a 561% increase. North Carolina alone went from $1.9 million to $505 million in five years, with projections approaching $1 billion by 2027.

- Rate cuts and hour reductions: In response to rising costs, some states are cutting reimbursement rates for ABA providers, which can push experienced providers out of the Medicaid network entirely.

- Tighter utilization management: Many states now require periodic chart reviews and prior authorization renewals to continue coverage. A child receiving 30 hours per week may face a review that reduces authorized hours mid-treatment.

- Fraud scrutiny: As Medicaid ABA spending grew rapidly, so did scrutiny of billing practices. This has led to investigations and policy changes that, unfortunately, can create delays for legitimate families too.

| State trend | Impact on families |

|---|---|

| Medicaid rate cuts | Fewer providers willing to accept Medicaid |

| Hour caps added | Children may lose authorized therapy time |

| Tighter prior auth | Delays in starting or continuing treatment |

| Provider audits | Some clinics reduce caseloads or close |

The debate over controlling autism therapy costs involves genuine policy tensions. Some policy analysts and researchers argue that mandated coverage has created incentives for over-diagnosis or overprescribing of intensive ABA hours. Others push back strongly, pointing out that restricting access harms children who need consistent, early intervention most. The letters to the editor debate following coverage of these issues in 2026 showed parents, clinicians, and researchers deeply divided on how policy should respond.

What this means for your family is straightforward: the rules governing your child’s therapy could change within a single budget cycle. Families who stay informed and engaged have a real advantage.

Many children also have access to services through the Individuals with Disabilities Education Act (IDEA), which funds school-based autism care separately from health insurance. Combining school services with your insurance benefits is one of the most effective cost-control strategies available to families.

Smart strategies for getting the most from your insurance

Understanding the system is only half the battle. The other half is using it strategically. Here are the steps families who successfully access autism care consistently take:

- Get a formal diagnosis as early as possible. Insurance requires a documented ASD diagnosis from a qualified clinician before approving any autism-specific therapies. The earlier this happens, the sooner coverage can begin and the more effective early intervention tends to be.

- Request a comprehensive written treatment plan. Your child’s treatment team, which may include a behavioral analyst (BCBA), pediatrician, or developmental pediatrician, should create a detailed plan that specifies the therapies needed, the hours recommended per week, and the clinical goals. This document is the foundation for every insurance claim.

- Know your plan’s prior authorization process. Almost every insurer requires prior authorization (pre-approval) before ABA therapy starts. Missing this step is one of the most common reasons coverage gets denied after services begin.

- Combine insurance with school IDEA services. Under federal law, children with ASD who qualify for special education services can receive related services through their school’s Individualized Education Program (IEP). An IEP paired with insurance coverage means more services without proportionally higher out-of-pocket costs.

- Use Medicaid waiver programs if eligible. Many states offer Home and Community Based Services (HCBS) waivers that provide additional autism services outside of standard Medicaid. Waitlists can be long, so apply early even if your child is young.

- Appeal every denial. Insurance denials are not final. When a claim is denied, you have the legal right to appeal. Get a letter from your doctor stating medical necessity, reference the EPSDT or ACA requirements that apply, and submit within the deadline. Organizations like Autism Speaks offer appeals guidance that can significantly improve your chances of success.

- Monitor your state legislature. Insurance mandates can be added, strengthened, or weakened through state law. Signing up for alerts from autism advocacy groups in your state keeps you ahead of changes that could affect your benefits.

Pro Tip: Keep a dedicated folder, digital or physical, for every piece of paperwork related to your child’s autism care. This includes prior authorization approvals, denial letters, treatment plans, and correspondence with your insurer. Organized documentation is your strongest tool when disputes arise.

Why navigating insurance for autism care requires more than paperwork

Here is something the insurance guides rarely tell you: having coverage does not guarantee timely, high-quality care. This is the uncomfortable reality that too many families discover after spending months fighting for approvals, only to find the real obstacle is getting an appointment.

Rising costs and fraud concerns have pushed both Medicaid programs and private insurers toward tighter utilization management. Families are reporting mid-treatment hour reductions after chart reviews, providers leaving Medicaid networks because reimbursement rates no longer cover operating costs, and waitlists stretching six months to over a year even in metropolitan areas. Having an active insurance card does not move you up a waitlist.

The deeper issue is that the current system measures therapy in volume rather than outcomes. Forty hours per week sounds like comprehensive care, but if the provider is not well-matched to your child, those hours may not produce the progress your child deserves. The shift toward value-based care models, which tie payment to measurable outcomes rather than hours logged, is gaining traction. Families who ask providers about specific outcome tracking and goal measurement often report better experiences, because they are selecting providers who think this way already.

Our honest take: treat your insurance approval as the beginning, not the destination. While you are in the authorization process, start building a shortlist of providers and get on waitlists immediately. Talk to other autism parents in your area. Local knowledge about which providers genuinely deliver results, and which ones are simply available, is information no insurance card can give you. Connecting with addressing provider shortages resources in your region is a practical next step that runs parallel to your insurance strategy, not after it.

Find trusted autism therapy providers and support

Knowing your rights and filing the right paperwork is essential, but you still need to find the right people to actually work with your child. That is exactly what the Autism Doctor Search Directory is built for. You can find autism therapy services vetted and listed in one place, including ABA providers, occupational therapists, mental health services, and special education schools. Providers like The Missing Piece ABA Therapy and Autism Therapeutics are among the resources families across the US have used to connect insurance benefits with quality, hands-on care. Stop searching one clinic at a time. Start with a directory that does the filtering for you.

Frequently asked questions

Does every health insurance plan in the US cover autism therapy?

Most Marketplace and small-group plans must cover autism therapies like ABA by law, but coverage details and limits vary by state and plan. The ACA requires essential health benefits coverage for behavioral health treatment, though self-funded employer plans may follow different rules.

Is there an age limit for autism therapy under Medicaid?

Federal law requires Medicaid to cover autism treatments for medically necessary cases under age 21, with no hard age or hour limits. Under EPSDT, coverage is need-based, not subject to arbitrary caps on hours or dollars.

What can I do if my insurance denies autism therapy coverage?

You can file an appeal, gather supporting documentation from your child’s doctor, and work with advocacy organizations for guidance. Advocacy resources like Autism Speaks provide specific support for overturning denials and navigating the appeals process.

Why are some families still struggling to access care even with insurance?

Provider shortages, long waitlists, and state-imposed limits can delay or restrict access even for insured families. Tighter utilization management driven by rising costs means approvals can be reduced or delayed mid-treatment, regardless of what your plan technically covers.

Will insurance always cover the full cost of autism care?

Insurance reduces costs significantly, but most families still owe deductibles, copays, or coinsurance. In some states, plan caps exist that may limit intensive therapy to only a portion of the recommended hours, leaving families to bridge the gap through other funding sources.